S-1: General form for registration of securities under the Securities Act of 1933

Published on

As filed with the Securities and Exchange Commission on April 13, 2026.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

___________________________

Rare Earths Americas, Inc.

(Exact name of registrant as specified in its charter)

___________________________

Texas |

|

1000 |

|

39-4918133 |

|

(State or other jurisdiction of incorporation or organization) |

|

(Primary Standard Industrial Classification Code Number) |

|

(I.R.S. Employer Identification Number) |

|

101 W. Main Street

Manchester, GA 31816

(706) 846-5063

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

___________________________

Donald Swartz

Chief Executive Officer and President

Rare Earths Americas, Inc.

101 W. Main Street

Manchester, GA 31816

(706) 846-5063

(Name, address, including zip code, and telephone number, including area code, of agent for service)

___________________________

Copies to:

Era Anagnosti Andrew Ledbetter DLA Piper LLP (US) 500 Eighth Street, NW Washington, D.C. 20004 (202) 799-4000 |

|

|

|

James Guttman Dorsey & Whitney LLP TD Bank Tower 66 Wellington Street W, Suite 3400 Toronto, ON M5K 1E6 (416) 367-7370 |

___________________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

☒ |

|

|

|

|

Emerging growth company |

|

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS |

|

SUBJECT TO COMPLETION, DATED , 2026 |

Shares

Common Stock

RARE EARTHS AMERICAS, INC.

This is the initial public offering of shares of common stock of Rare Earths Americas, Inc. All of the shares of common stock are being sold by us.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to apply to list our common stock on the NYSE American LLC (“NYSE American”) under the trading symbol “REA”.

We are an “emerging growth company” and a “smaller reporting company” as defined under the federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this prospectus and may elect to do so in future filings.

Investing in our common stock involves a high degree of risk. See the section titled “Risk Factors” beginning on page 11 to read about factors you should consider before buying shares of our common stock.

|

|

Per share |

|

Total |

|

||

Initial public offering price |

|

$ |

|

|

$ |

|

|

Underwriting discounts(1) |

|

$ |

|

|

$ |

|

|

Proceeds to us before expenses(2) |

|

$ |

|

|

$ |

|

|

____________

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares of common stock from us at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2026.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Cantor Stifel

B. Riley Securities Canaccord Genuity

Prospectus dated , 2026

TABLE OF CONTENTS

|

|

|

Page |

|

|

1 |

|

|

|

6 |

|

|

|

8 |

|

|

|

9 |

|

|

|

11 |

|

|

|

42 |

|

|

|

44 |

|

|

|

46 |

|

|

|

47 |

|

|

|

48 |

|

|

|

50 |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

|

52 |

|

|

64 |

|

|

|

95 |

|

|

|

127 |

|

|

|

134 |

|

|

|

144 |

|

|

|

146 |

|

|

|

148 |

|

|

|

153 |

|

Material U.S. Federal Income Tax Consequences to Non-U.S. Holders |

|

|

155 |

|

|

159 |

|

|

|

170 |

|

|

|

170 |

|

|

|

170 |

|

|

|

F-1 |

“REA,” “Rare Earths Americas,” the “Rare Earths Americas” logo, and other trademarks, trade names, or service marks of Rare Earths Americas, Inc. appearing in this prospectus are the property of Rare Earths Americas, Inc. All other trademarks, trade names, and service marks appearing in this prospectus are the property of their respective owners. Solely for convenience, the trademarks and trade names in this prospectus may be referred to without the ® and ™ symbols, but such references should not be construed as any indicator that their respective owners will not assert their rights thereto.

Neither we nor the underwriters have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, and results of operations may have changed since that date.

For investors outside the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus and any such free writing prospectus outside the United States.

i

PROSPECTUS SUMMARY

This summary highlights selected information contained in greater detail elsewhere in this prospectus. This summary is not complete and does not contain all of the information you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including the sections titled “Risk Factors,” “Special Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes included elsewhere in this prospectus. As used in this prospectus, unless the context otherwise requires, references to “we,” “us,” “our,” “the Company,” “REA,” “Rare Earths Americas” and similar references refer to Rare Earths Americas, Inc. together with its consolidated subsidiaries.

Overview

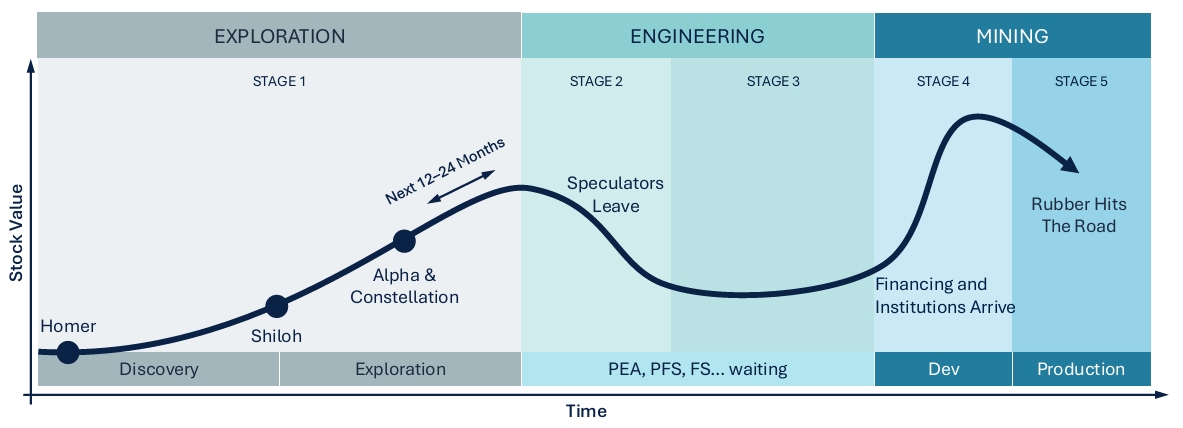

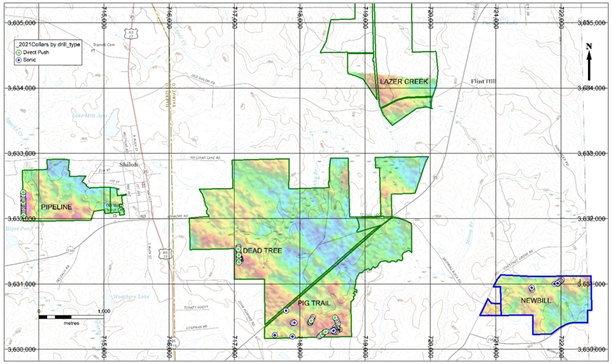

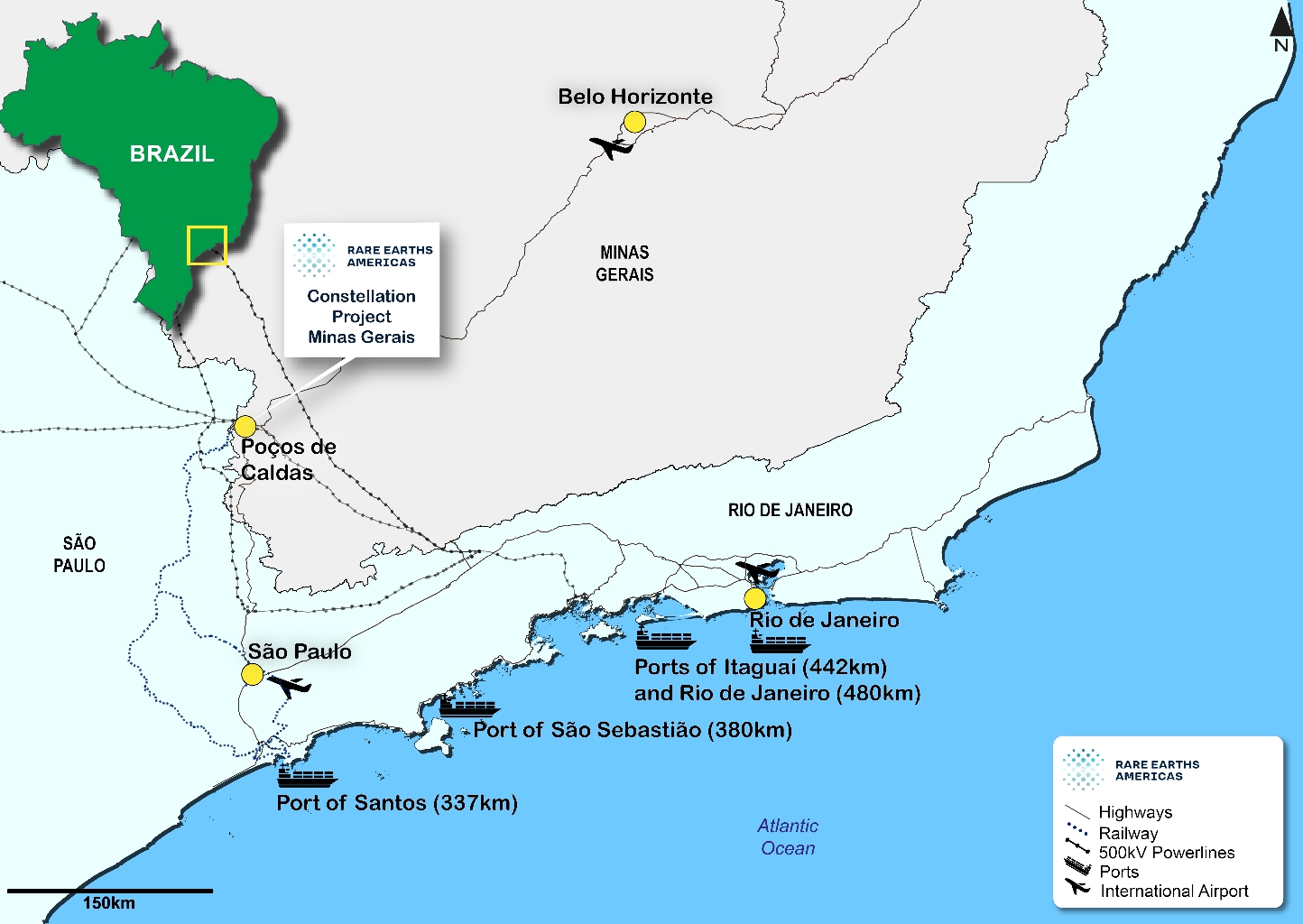

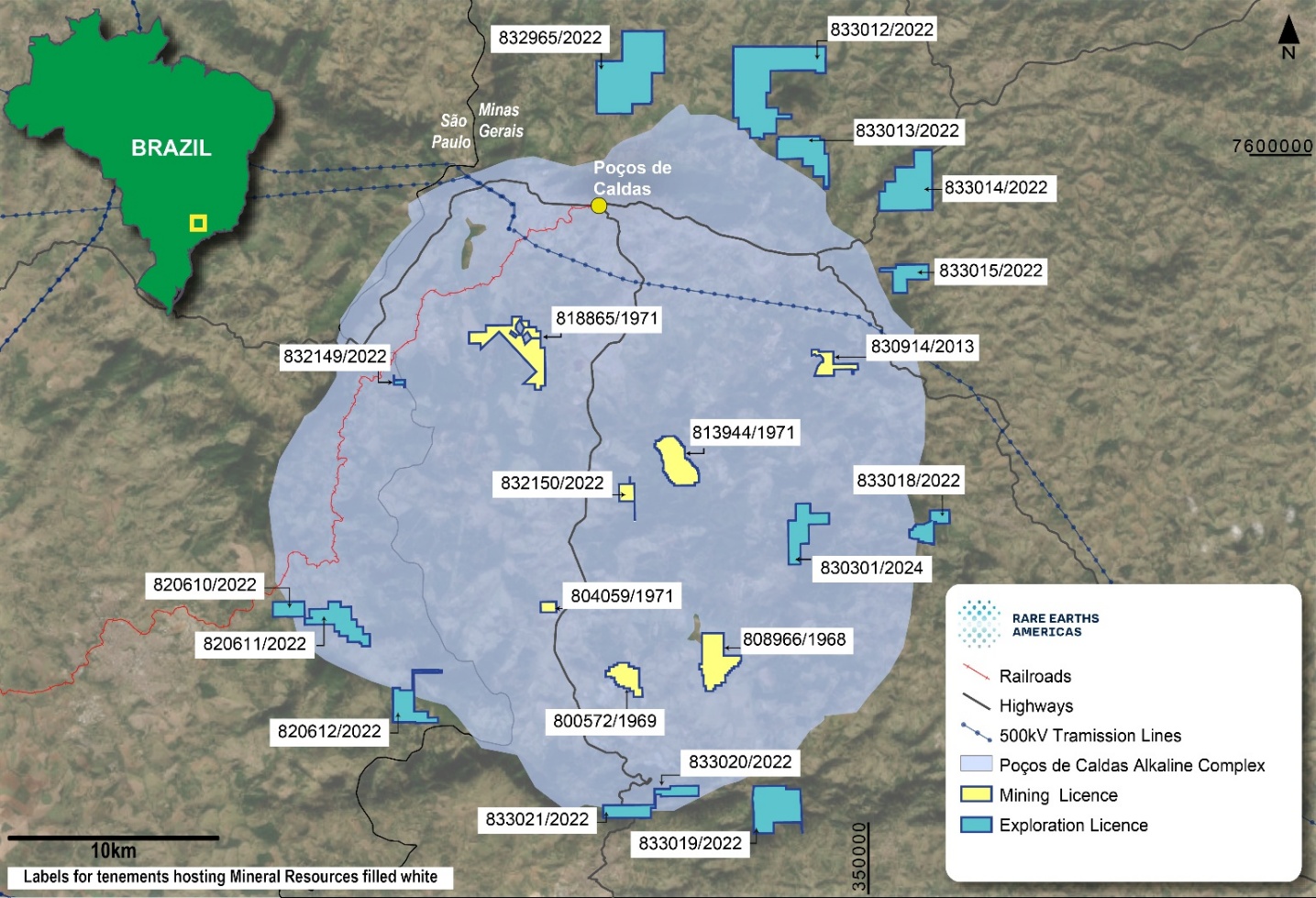

We are an exploration stage company advancing a portfolio of critical minerals projects focused on high-grade heavy rare earth mineral assets. Our work is aimed toward defining mineralization for our projects and increasing our understanding of its characteristics and economics. Our portfolio includes three material projects, which we believe positions REA as a future potential cornerstone of non-Chinese rare earth supply, aligning with Western industrial and national security priorities:

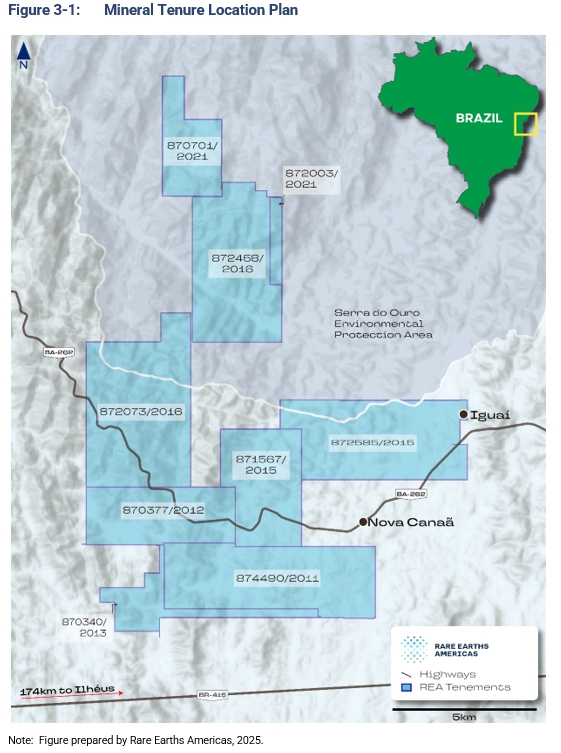

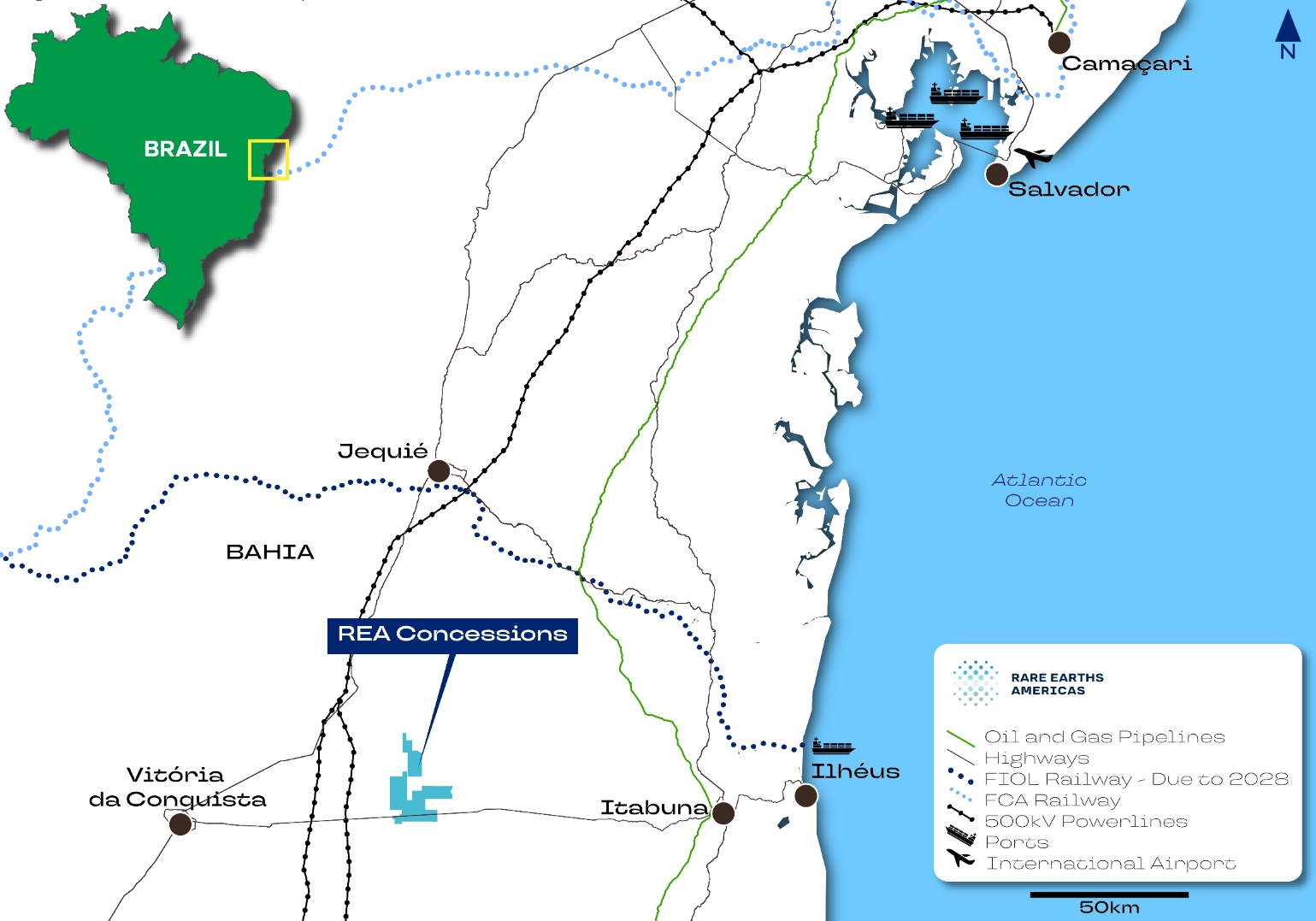

We also hold rights to several additional, currently not material, early-stage exploration projects, most notably our Homer Project located in Goiás, Brazil, and Liberty Peak located in Georgia, United States. The Homer Project hosts multiple large carbonatite clusters with potential for rare earth minerals and niobium considering the region contains

1

some of the world’s preeminent niobium mines. During the first quarter of 2026, we started an active drilling campaign at Homer, based on field work, sampling and prospecting work performed in 2024 and 2025. We control 1,233 km² of tenements in Brazil. Liberty Peak is a new discovery zone within the Shiloh Project area, with recent prospecting confirming monazite-sands at the surface. We recently completed an airborne geophysical and magnetic survey over approximately 500 km2 of Liberty Peak and plan to accelerate exploration at Liberty Peak throughout 2026, including land acquisition, future drilling, and opening of a satellite facility.

Our primary focus is on heavy rare earth elements, which are critical to high-performance permanent magnets used in robotics, defense applications, electric vehicles, wind power systems, renewable energy systems, and consumer electronics. We are currently in the exploration stage, with no revenue generated to date. Our objective is to systematically advance our portfolio—comprising the Shiloh Project, the Alpha Project, and the Constellation Project—from early exploration toward resource definition and, eventually, development.

Our projects are strategically positioned, with dual-jurisdiction exposure in the United States and Brazil, which aligns with growing initiatives in the U.S. and its cooperating nations to ensure diversified, secure rare earth elements supply chains.

Our Business Strategy

We intend to grow the value of our assets by:

We believe the long-term prospects for rare earth elements, more specifically heavy rare earth elements, continue to be strong, as described in more detail in the section titled “Business.” In part, this reflects the acknowledgment of the U.S. Government that critical minerals, including rare earth elements, are essential for national security and economic resilience and its policies to facilitate domestic mineral production, including by offering expedited permitting, reconsidering regulatory bottlenecks, and providing capital and technical assistance. We have assembled a team with extensive mining sector-related experience, including exploration, development, permitting, operations and capital markets, to execute our strategy and pursue the market opportunity available to us.

Corporate Information

We were incorporated in February 2025 under the laws of the Cayman Islands as “Rare Earths Americas Ltd.” We completed a redomestication transaction through the filing of a certificate of conversion, becoming a Texas corporation on October 15, 2025 (the “Redomestication”). Following the Redomestication, our name changed to “Rare Earths Americas, Inc.”

In July 2025, in two transactions, each contingent upon the completion of the other, we acquired our predecessor, Alpha Minerals Brazil Participações Ltda., a company organized under the laws of Brazil (“AMBPL” or “Predecessor”), and Foothills Rare Earths Limited, an Australian public unlisted corporation (“FRE Australia”). Consideration paid to the shareholders of AMBPL and FRE Australia consisted of shares of our common stock and warrants exercisable for shares of our common stock. REA and AMBPL were entities under common control at the acquisition date.

2

We operate and control our business and affairs through our wholly owned subsidiaries: AMBPL, FRE Australia, Foothills Rare Earths LLC (“FRE US”), and T.E. Liberty Holdings, LLC (“T.E. Liberty”).

Our principal executive offices are located at 101 W. Main Street, Manchester, Georgia 31816. In support of our exploration activities, we also maintain field offices in the state of Georgia and in Brazil. Our corporate website is rareearthsamericas.com. Information contained on, or accessible through, our website shall not be deemed incorporated by reference and is not a part of this prospectus or the registration statement of which it forms a part. We have included our website in this prospectus solely as an inactive textual reference and do not intend it to be an active link to our website.

Risk Factors

Our business is subject to a number of risks of which you should be aware before making a decision to invest in our common stock. These risks are more fully described in the section titled “Risk Factors” immediately following this prospectus summary. These risks include, among others, the following:

3

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may take advantage of relief from certain reporting requirements and other burdens that are otherwise applicable generally to public companies. These provisions include:

4

In addition, under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We intend to avail ourselves of this exemption from new or revised accounting standards, and accordingly, we will not be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies or that have opted out of using such extended transition period, which may make comparison of our financial statements with those of other public companies more difficult. We may take advantage of these reporting exemptions until we no longer qualify as an emerging growth company or, with respect to adoption of certain new or revised accounting standards, until we irrevocably elect to opt out of using the extended transition period.

We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year in which we have total annual gross revenue of $1.235 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the closing of this offering; (iii) the date on which we have issued more than $1 billion in nonconvertible debt during the previous three years; and (iv) the date on which we are deemed to be a large accelerated filer under the rules of the SEC. We may choose to take advantage of some but not all of these reduced reporting burdens.

We are also a “smaller reporting company,” meaning that the market value of our stock held by non-affiliates plus the proposed aggregate amount of gross proceeds to us as a result of this offering is less than $700.0 million and our annual revenue is less than $100.0 million during the most recently completed fiscal year. We may continue to be a smaller reporting company after this offering if either (i) the market value of our stock held by non-affiliates is less than $250.0 million or (ii) our annual revenue is less than $100.0 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700.0 million. If we are a smaller reporting company at the time we cease to be an emerging growth company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. Specifically, as a smaller reporting company we may choose to present only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K and, similar to emerging growth companies, smaller reporting companies have reduced disclosure obligations regarding executive compensation.

5

THE OFFERING

Common stock offered by us |

|

shares |

Underwriters’ option to purchase additional shares of common stock |

|

We have granted the underwriters a 30-day option to purchase up to additional shares of common stock at the initial public offering price less the underwriting discounts. |

Common stock to be outstanding immediately after this offering |

|

shares ( shares if the underwriters exercise their over-allotment option in full). |

Use of proceeds |

|

We estimate that the net proceeds from this offering will be approximately $ million (or approximately $ million if the underwriters exercise in full their option to purchase up to additional shares of common stock), after deducting the underwriting discounts and estimated offering expenses payable by us. We intend to use the net proceeds from this offering as follows: • approximately $ million to fund land acquisition and option payments, drilling, metallurgical test work, permitting and S-K 1300 technical report summary preparation at our Shiloh Project. We plan to prioritize advancement of our Shiloh Project; • approximately $ million to fund exploration, evaluation, land consolidation, metallurgy, engineering and permitting studies at our Alpha Project; and • approximately $ million to fund exploration, evaluation, land option payments, metallurgy, engineering and permitting studies at our Constellation Project. We intend to use any remaining net proceeds for evaluating our non-material exploration projects, including Homer and Liberty Peak, as well as for working capital and other general corporate purposes. See the section titled “Use of Proceeds” for additional information. We may find it necessary or advisable to use the net proceeds for other purposes, and our management will have broad discretion in the application of the net proceeds, and investors will be relying on our judgment regarding the application of the net proceeds from this offering. |

Lock-up |

|

We have agreed, subject to certain exceptions and without the approval of Cantor, not to offer, issue, sell, contract to sell, encumber, grant any option for the sale of, or otherwise dispose of any of our securities for a period of 180 days following the closing of this offering. Our directors, executive officers, and a significant portion of all other holders of our common stock prior to this offering have agreed with the underwriters not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of our common stock or securities convertible into common stock for a period of 180 days following the closing of this offering, subject to certain exceptions. See the section titled “Underwriting” for additional information. |

Risk factors |

|

See “Risk Factors” on page 11 and other information included in this prospectus for a discussion of factors to consider carefully before deciding to invest in our securities. |

Proposed NYSE American symbol |

|

REA |

The number of shares of our common stock to be outstanding after this offering is based on shares of common stock outstanding as of , 2026 and excludes:

6

Our 2026 Plan provides for annual automatic increases in the number of shares reserved thereunder. See the section titled “Executive Compensation—Equity Incentive Plans” for additional information.

Unless otherwise indicated, all information contained in this prospectus, including the number of shares of common stock that will be outstanding after this offering, assumes or gives effect to:

7

SUMMARY FINANCIAL DATA

The following tables set forth a summary of our historical financial data. The selected consolidated statements of operations data for the years ended December 31, 2025 and 2024, and the selected consolidated statements of cash flows data for the years ended December 31, 2025 and 2024 have been derived from our consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future.

You should read the following summary financial data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes included elsewhere in this prospectus. The summary financial data in this section are not intended to replace, and are qualified in their entirety by, the financial statements and related notes. Dollars presented in thousands, except per share data.

|

|

For the Year Ended December 31, |

|

|||||

|

|

2025 |

|

|

2024 |

|

||

|

|

|

|

|

|

|

||

Operating expenses: |

|

|

|

|

|

|

||

Exploration and evaluation expenses |

|

$ |

3,717 |

|

|

$ |

2,890 |

|

General and administrative expenses |

|

|

5,466 |

|

|

|

1,094 |

|

Depreciation expense |

|

|

25 |

|

|

|

6 |

|

Transaction costs |

|

|

247 |

|

|

|

— |

|

Total operating expenses |

|

|

9,455 |

|

|

|

3,990 |

|

Operating loss |

|

|

(9,455 |

) |

|

|

(3,990 |

) |

Other income (expenses): |

|

|

|

|

|

|

||

Interest income |

|

|

138 |

|

|

|

15 |

|

Interest expense |

|

|

(206 |

) |

|

|

— |

|

Foreign exchange gain |

|

|

31 |

|

|

|

— |

|

Loss on extinguishment of debt |

|

|

(577 |

) |

|

|

— |

|

Change in fair value of warrants |

|

|

139 |

|

|

|

— |

|

Total other (expenses) income |

|

|

(475 |

) |

|

|

15 |

|

Loss before income taxes |

|

|

(9,930 |

) |

|

|

(3,975 |

) |

Provision for income taxes |

|

|

— |

|

|

|

— |

|

Net loss |

|

|

(9,930 |

) |

|

|

(3,975 |

) |

Less: Net loss attributable to noncontrolling interest |

|

|

— |

|

|

|

— |

|

Net loss attributable to Rare Earths Americas, Inc. |

|

$ |

(9,930 |

) |

|

$ |

(3,975 |

) |

Net loss per common share, basic and diluted |

|

$ |

(0.85 |

) |

|

$ |

(0.46 |

) |

Weighted average common shares outstanding, basic and diluted |

|

|

11,744,438 |

|

|

|

8,674,507 |

|

|

|

Year Ended December 31, |

|

|||||

|

|

2025 |

|

|

2024 |

|

||

Other Financial Data (in thousands): |

|

|

|

|

|

|

||

Net cash used in operating activities |

|

$ |

(4,855 |

) |

|

$ |

(3,793 |

) |

Net cash provided by investing activities |

|

|

1,063 |

|

|

|

65 |

|

Net cash provided by financing activities |

|

|

26,547 |

|

|

|

3,311 |

|

8

GLOSSARY OF MINING AND OTHER TERMS

“Cut-off Grade” means a term used in S-K 1300 to describe the grade that determines the destination of the material during mining. For purposes of establishing “prospects of economic extraction,” the cut-off grade is the grade that distinguishes material deemed to have no economic value (it will not be mined in underground mining or if mined in surface mining, its destination will be the waste dump) from material deemed to have economic value (its ultimate destination during mining will be a processing facility).

“Deposit” means an accumulation of minerals.

“Development Stage” means a term used in S-K 1300 to describe a property that has mineral reserves disclosed but no material extraction.

“Exploration Stage” means a term used in S-K 1300 to describe a property that has no mineral reserves disclosed.

“Feasibility Study” means a term used in S-K 1300 to describe a comprehensive technical and economic study of the selected development option for a mineral project, which includes detailed assessments of all applicable modifying factors, as defined by S-K 1300, together with any other relevant operational factors, and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is economically viable. The results of the study may serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project.

“Indicated Mineral Resource” means a term used in S-K 1300 to describe that part of a mineral resource for which quantity and grade or quality are estimated on the basis of adequate geological evidence and sampling. The level of geological certainty associated with an indicated mineral resource is sufficient to allow a qualified person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Because an indicated mineral resource has a lower level of confidence than the level of confidence of a measured mineral resource, an indicated mineral resource may only be converted to a probable mineral reserve.

“Inferred Mineral Resource” means a term used in S-K 1300 to describe that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. The level of geological uncertainty associated with an inferred mineral resource is too high to apply relevant technical and economic factors likely to influence the prospects of economic extraction in a manner useful for evaluation of economic viability. Because an inferred mineral resource has the lowest level of geological confidence of all mineral resources, which prevents the application of the modifying factors in a manner useful for evaluation of economic viability, an inferred mineral resource may not be considered when assessing the economic viability of a mining project, and may not be converted to a mineral reserve.

“Measured Mineral Resource” means a term used in S-K 1300 to describe that part of a mineral resource for which quantity and grade or quality are estimated on the basis of conclusive geological evidence and sampling. The level of geological certainty associated with a measured mineral resource is sufficient to allow a qualified person to apply modifying factors, as defined in S-K 1300, in sufficient detail to support detailed mine planning and final evaluation of the economic viability of the deposit. Because a measured mineral resource has a higher level of confidence than the level of confidence of either an indicated mineral resource or an inferred mineral resource, a measured mineral resource may be converted to a proven mineral reserve or to a probable mineral reserve.

“Mineralization” means the concentration of metals within a body of rock or the process by which such concentration occurs.

“Mineral Reserve” means a term used in S-K 1300 to describe an estimate of tonnage and grade or quality of indicated and measured mineral resources that, in the opinion of a qualified person, can be the basis of an economically viable project. More specifically, it is the economically mineable part of a measured or indicated mineral resource, which includes diluting materials and allowances for losses that may occur when the material is mined or extracted.

9

“Mineral Resource” means a term used in S-K 1300 to describe a concentration or occurrence of material of economic interest in or on the Earth’s crust in such form, grade or quality, and quantity that there are reasonable prospects for economic extraction. A mineral resource is a reasonable estimate of mineralization, taking into account relevant factors such as cut-off grade, likely mining dimensions, location or continuity, that, with the assumed and justifiable technical and economic conditions, is likely to, in whole or in part, become economically extractable. It is not merely an inventory of all mineralization drilled or sampled.

“Mining” means the extraction of valuable geological materials from the Earth.

“Probable Mineral Reserves” means a term used in S-K 1300 to describe the economically mineable part of an indicated and, in some cases, a measured mineral resource.

“Qualified Person” or “QP” means a term used in S-K 1300 to describe an individual who (1) is a mineral industry professional with at least five years of relevant experience in the type of mineralization and type of deposit under consideration and in the specific type of activity that person is undertaking on behalf of us; and (2) is an eligible member or licensee in good standing of a recognized professional organization that meets certain criteria specified under S-K 1300.

“Recovery” means that portion (usually expressed as a percentage) of the metal contained in mineralized material that is successfully extracted by processing.

“Sampling” means selecting a fractional part of a mineral deposit for analysis.

“Sediment” means solid fragmental material that originates from weathering of rocks and is transported or deposited by air, water, or ice, or that accumulates by other natural agents, such as chemical precipitation from solution or secretion by organisms, and that forms in layers on the earth’s surface at ordinary temperatures in a loose, unconsolidated form.

“S-K 1300” means subpart 1300 of Regulation S-K, promulgated by the U.S. Securities and Exchange Commission, which sets forth the rules and regulations for disclosure by registrants engaged in the mining industry.

“Technical Report Summaries” means, collectively, the technical report summaries for each of the Shiloh Project, Alpha Project and Constellation Project, in accordance with S-K 1300, filed as Exhibits 96.1, 96.3 and 96.2, respectively, to this registration statement, of which this prospectus forms a part.

“TREO” means total rare earth oxides.

10

RISK FACTORS

In addition to the other information contained in this prospectus, including the matters addressed under the heading “Special Note Regarding Forward-Looking Statements” and “Market and Industry Data,” you should carefully consider the following risk factors, together with all of the other information included in this prospectus, including the financial statements and notes to the financial statements included herein, before deciding whether to invest in our common stock. The risk factors described below disclose the material risks, but are not intended to be exhaustive, and do not describe all of the risks we are facing or may face in the future. The occurrence of one or more of the events or circumstances described in these risk factors, alone or in combination with other events or circumstances, may have a material adverse effect on our business, financial condition, results of operations and prospects of, in which event the market price of our common stock could decline, and you could lose part or all of your investment. Additional risks not currently known to us or that we currently deem to be immaterial, or that are not identified because they are generally common to businesses, also may have a material adverse effect on our business, financial condition, results of operations or prospects. Because of the factors described in this section and elsewhere in this prospectus, as well as other factors affecting our businesses, financial condition, operating results, and prospects, past financial performance should not be considered a reliable indicator of future performance, and investors should not rely on historical trends to anticipate trends or results in the future.

Risks Related to Our Business

We are an exploration stage mining company with no operating history other than conducting limited exploratory activities, and there are no assurances that we will build successful business operations or ever produce minerals from any of our properties.

We are an exploration stage mining company, which means that we have no material property with mineral reserves disclosed. We do not currently operate any mines, and we do not have any direct or indirect interest in any active mining operations. Each of our three material mineral projects, the Shiloh Project, Alpha Project, and Constellation Project, is in an exploration stage and has never been mined for rare earth elements by us or by any prior owner. Additionally, we have several additional, currently not material, early-stage exploration projects, including our Homer Project and Liberty Peak. As a result, we have never produced revenue, and we have no operating history upon which to base estimates of future operating costs, capital expenditure needs, site remediation costs or other necessary investments. While our management team and board of directors have extensive combined mining sector-related experience, the Company has no experience in developing or operating a mine.

We may never be able to develop and produce minerals from a commercially viable mineral property. Although we continue systematic exploration of our properties, such as the Shiloh Project, results of these exploratory works are not yet available and there is no certainty that such results will be consistent with the earlier results disclosed herein.

Advancing our mineral properties to the development stage (which the SEC defines as the preparation of mineral reserves for extraction) will require significant capital and time, and successful commercial production from any mines will be subject to the additional risks associated with developing and establishing new mining operations and business enterprises including:

11

Our mining rights are subject to mineral rights purchase option agreements, and we may be unable to exercise such options.

Our wholly owned subsidiaries are party to various mineral rights purchase option agreements, pursuant to which we have been granted options to purchase and/or lease certain mining rights subject to, among other things, our payment of the applicable premiums and exercise prices, which are substantial. Therefore, our acquisition of certain mining rights depends on our ability to obtain adequate financial resources to pay the applicable exercise prices. In some instances, the payment of the exercise price shall be via the issuance of our shares, which issuance would dilute the ownership percentage of existing stockholders. We may not be able to successfully complete our planned exploration activities, establish mining operations or profitably produce rare earth elements at any of our current or future properties if we are unable to exercise such options. Please see the section titled “Business – Mining Rights” for a description of our mineral rights purchase option agreements. In addition, any impairment in the value of these mineral interests could negatively impact our business and cause the price of our common stock to decline.

We have no history of producing rare earth elements.

We have no history of producing rare earth elements. Our properties are all exploration stage properties in various stages of exploration and evaluation. Our Shiloh Project and our non-material exploration projects, including Homer and Liberty Peak, are all early-stage exploration projects and are not yet at the resource stage. Advancing properties from exploration into the development stage requires significant capital and time, and successful commercial production from a property, if any, will be subject to completing various studies through definitive feasibility, permitting and construction of the mines, processing plants, roads, and other related works and infrastructure. As a result, we are subject to all the risks associated with developing and establishing new mining operations and business enterprises including:

12

The costs, timing and complexities of exploration, development and construction activities may be increased by the location of our properties and demand by other rare earth elements exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if warranted, development, construction and mine start-up. Accordingly, our activities may not result in profitable mining operations and we may not succeed in establishing mining operations or profitably producing rare earth minerals.

Mineral exploration is highly speculative and subject to an exceptionally high probability of failure.

The mineral exploration industry is characterized by significant risk and uncertainty. It is widely understood that many exploration programs are unsuccessful for a multitude of reasons including political environment, capital markets, lack of funding and government regulation.

The purpose of exploration is to demonstrate the dimensions, position and mineral characteristics of mineral deposits, estimate mineral resources, assess amenability of the deposit to mining and processing scenarios and estimate potential deposit value. Once mineralization is discovered, it may take several years from the initial exploration phases before production is possible, during which time the project may cease to be feasible. Substantial expenditures are required to establish proven and probable mineral reserves, to determine processes to extract the metals and, if required, to construct mining and processing facilities and obtain the rights to the land and resources required to develop the mining activities.

Development projects have no operating history upon which to base estimates of proven and probable mineral reserves and estimates of future operating costs. Estimates are, to a large extent, based upon the interpretation of geological data and modeling obtained from drill holes and other sampling techniques, feasibility studies that derive estimates of operating costs based upon anticipated tonnage and grades of material to be mined and processed, the configuration of the deposit, expected recovery rates, facility and equipment capital and operating costs, anticipated climatic conditions and other factors. As a result, actual operating costs and economic returns based upon development of proven and probable mineral reserves may differ significantly from those originally estimated. Moreover, significant decreases in actual or expected commodity prices may mean rare earth elements, once found, will be uneconomical to mine.

We have not yet established mineral reserves and hold exploration options that may not mature into viable operations. There is no guarantee that the properties contain economically extractable rare earth elements, or that we will be able to bring such properties to economic production.

Estimates that guide our development plans and anticipated financing needs with respect to our mineral projects may prove inaccurate or incomplete, which could adversely affect our ability to continue our exploration plans and to profitably produce rare earth elements at any of our properties.

Estimates that guide our development and financing plans are based on the interpretation of geological data, feasibility studies, anticipated climatic conditions and other factors. Any of the following events, among the other events and uncertainties described in this prospectus, could affect the accuracy of such estimates:

13

Inaccuracies in such estimates could adversely affect our ability to continue our exploration plans and to profitably produce rare earth elements at any of our current or future properties.

Any material changes in mineralization estimates and grades of mineralization will affect the economic viability of placing any projects into production.

Because we have not completed various studies and have not commenced actual production, mineralization estimates for our projects may require adjustments or downward revisions. Rare earth elements recovered in small scale tests may not be duplicated in large scale tests under on-site conditions or in production scale. Moreover, while we continue systematic exploration of our properties, such as the Shiloh Project, results of these exploratory works are not yet available, and may be significantly delayed due to the limited availability of laboratories to process and analyze assay results and there is no certainty that such results will be consistent with results disclosed in this prospectus.

The estimates contained in this prospectus have been determined and valued based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for rare earth elements may render portions of our mineralization estimates uneconomic and result in reduced reported mineralization or adversely affect the commercial viability determinations we reach. Any material reductions in estimates of mineralization, or of our ability to extract this mineralization, could have a material adverse effect on our share price and the value of our properties.

We may be adversely affected by fluctuations in demand for, and prices of, magnet rare earth elements.

Because our potential revenue is, and will for the foreseeable future be, derived from the production and sale of rare earth elements, changes in demand for, and the market price of, and taxes and other tariffs and fees imposed upon magnet rare earth elements and their inputs could significantly affect our profitability. Our financial results may be significantly adversely affected by declines in the prices of magnet rare earth elements. Magnet rare earth elements prices may fluctuate and are affected by numerous factors beyond our control, such as interest rates, exchange rates, taxes, tariffs, inflation or deflation, fluctuation in the relative value of the U.S. dollar against foreign currencies on the world market, shipping and other transportation and logistics costs, global and regional supply and demand for magnet rare earth elements, potential industry trends, such as competitor consolidation or other integration methodologies, and the political and economic conditions of countries that produce and procure magnet rare earth elements. Furthermore, supply side factors have a significant influence on price volatility for critical and rare earth elements prices. Supply of rare earth elements is currently dominated by Chinese producers. The Chinese Central Government regulates production via quotas and environmental standards and has in the past and may continue to change in the future such production quotas and environmental standards. Periods of over supply or speculative trading of rare earth elements can lead to significant fluctuations in the market price of rare earth elements.

In contrast, extended periods of high commodity prices may create economic dislocations that may be destabilizing to rare earth elements supply and demand and ultimately to the broader markets. While some periods of high rare earth elements market prices generally are beneficial to our financial performance if we are producing rare earth elements, if ever, or if magnet rare earth elements prices rise in concert with such higher rare earth elements prices, strong rare earth elements prices, however, also create economic pressure to identify or create alternate technologies that ultimately could depress future long-term demand for magnet rare earth elements, and at the same time may incentivize development of competing mining properties.

The success of our business will depend, in part, on the growth of existing and emerging uses for magnet rare earth elements.

14

Our strategy is to produce and sell magnet rare earth elements, which are used in existing and emerging technologies, such as robotics, electric and hybrid vehicles, advanced air mobility, clean energy, consumer electronics and other high-growth, advanced motion technologies. The success of our business accordingly depends on the continued growth of these end markets and successfully commercializing magnet rare earth elements in such markets. If the market for these existing and emerging technologies does not grow as we expect, grows more slowly than we expect, or if the demand for our products in these markets decreases, then our business, prospects, financial condition and operating results could be harmed. In addition, the market for these technologies, particularly in the automotive and wind turbine industry, tends to be cyclical, which exposes us to increased volatility, and it is uncertain as to how such macroeconomic factors will impact our business.

A prolonged or significant economic contraction in the United States or worldwide could put downward pressure on market prices of magnet rare earth elements. Protracted periods of low prices for magnet rare earth elements could significantly reduce revenues and the availability of required development funds in the future. This could cause substantial reductions to, or a suspension of, magnet production operations, impair asset values and reduce our results of operations and financial condition.

Demand for our products may be impacted by demand for downstream products incorporating magnet rare earth elements, including robotics, hybrid and electric vehicles, wind turbines, medical equipment, military equipment and other high-growth, advanced motion technologies, as well as demand in the general automotive and electronic industries. Lack of growth or changes in these markets may adversely affect the demand for our products. Any unexpected costs or delays in the commercialization of magnet rare earth elements or any of our other expected products, or less than expected demand for the critical existing and emerging technologies that use magnet rare earth elements, could have a material adverse effect on our financial condition or results of operations.

An increase in the global supply of magnet rare earth elements or, dumping, predatory pricing and other tactics by our competitors or state actors may adversely affect our profitability.

The pricing and demand for magnet rare earth elements is affected by several factors beyond our control, including growth of economic development and the global supply and demand for magnet rare earth elements. China is projected to continue to account for a substantial portion of global magnet rare earth elements production in the near future. China dominates the manufacture of metals and magnet rare earth elements, capabilities that are not currently materially present in the United States, and the Chinese Central Government regulates production via quotas and environmental standards. Over the past few years, there has been significant restructuring of the Chinese markets in line with China Central Government policy. Assuming that we reach production of magnet rare earth elements and other planned downstream products and subsequently become fully operational and integrated, increased competition may lead our competitors to engage in predatory pricing or other behaviors designed to inhibit our further downstream integration. Any increase in the amount of magnet rare earth elements or related products available in the market, including those exported from other nations, would result in increased competition and may result in price reductions, reduced margins or loss of potential market share, any of which could materially adversely affect our profitability. As a result of these factors, we may not be able to compete effectively against current and future competitors.

A shortage of equipment, supplies and qualified personnel could adversely affect our ability to operate our business.

We are dependent on various supplies and equipment to carry out our mining exploration and, if warranted, development operations. The shortage of such supplies, equipment and parts could have a material adverse effect on our ability to carry out our operations and therefore limit or increase the cost of production.

Suitable infrastructure may not be available or damage to existing infrastructure may occur.

Exploration activities depend on adequate infrastructure. Reliable roads, bridges, port and/or rail transportation, power sources, water supply and access to key consumables are important determinants for capital and operating costs. The lack of availability on acceptable terms or the delay in the availability of any one or more of these items could prevent or delay exploration, development or exploitation of our projects. If adequate infrastructure is not available in a timely and cost-effective manner, the exploitation or development of our projects might not be commenced or completed on a timely basis, or at all, the resulting operations might not achieve the anticipated production volume and the construction costs and operating costs associated with the exploitation and/or development of our projects might be higher than anticipated. In addition, extreme weather phenomena, sabotage, vandalism, government, non-governmental organization and community or other interference in the maintenance or provision of such infrastructure could adversely affect our business, results of operations, financial condition or prospects.

15

Diminished access to water may adversely affect our operations.

Exploration and eventual processing of rare earth elements requires significant amounts of water. Any disruption in the process or loss of access to adequate water sources could prompt the need for significant access to fresh water. Additionally, once we complete the pending projects, we will require an even greater amount of water for our separation and extraction operations, including additional fresh water. In addition, water usage, including extraction, containment, and recycling, requires appropriate permits, which are granted by respective regulatory authorities in Brazil and the United States. The available water supply may be adversely affected by shortages or changes in governmental regulations. We cannot assure stockholders that water will be available in sufficient quantities to meet our future production needs or will prove sufficient to meet our water supply needs. In addition, we cannot assure stockholders that we will maintain our existing licenses related to water rights, particularly if political changes lead to additional regulatory requirements or review of existing licenses. A reduction in our water supply could materially adversely affect our business, results of operations and financial position. In addition, if we are unable to obtain the necessary licenses with respect to water use, we may be prevented from pursuing some of our planned expansion projects.

We depend on key personnel for the success of our business. We may be unable to attract and retain qualified mining and technical personnel, which could materially and adversely affect our business and the execution of our strategic plans.

We highly value and depend on the contributions of our senior management and key personnel, particularly our experts with respect to rare earth elements production. Our success continues to depend largely upon the performance of key officers, employees and consultants who have advanced us to our current stage and contributed to our potential for future growth. The mining industry in the United States faces a significant and growing shortage of skilled personnel, including qualified mining engineers, geologists, metallurgists, and experienced technical staff. The U.S. mining workforce has a high average age, and a substantial number of experienced professionals are expected to retire in the coming years. At the same time, enrollment in university and college mining engineering and geology programs has been in a long-term decline, leading to a limited pipeline of new talent.

Our ability to execute our exploration, development, and operational plans depends on our capacity to attract, hire, and retain individuals with the necessary technical skills and experience. As a result of this industry-wide shortage, we face increased competition for talent, which may require us to offer higher compensation packages or face delays in hiring. We may also be required to seek talent from foreign jurisdictions, which could be subject to visa and other immigration-related restrictions. We may not be able to replace our senior management or key personnel (including personnel that are key to rare earth elements production) with persons of equivalent expertise and experience within a reasonable period of time or at all if one or more of our senior management and key personnel are not retained, and we may incur additional expenses to recruit, train and retain additional personnel. Any prolonged inability to retain key individuals, or to attract and retain new talent as we grow, could have a material adverse effect upon our growth potential and prospects. Additionally, we have not purchased any “key-man” insurance for our directors, officers or key employees.

The loss of key personnel or our inability to find suitable replacements in a timely manner could:

If we are unable to successfully attract and retain a sufficient number of qualified employees, it could have a material adverse effect on our business, financial condition, and results of operations.

We may enter into contracts with government entities, which may expose us to greater risks than contracts with non-government entities.

16

We may enter into contracts with government entities. The terms of such contracts are often non-negotiable and may expose us to greater commercial, political and operational risks than we would assume in other contracts, such as, for example, exposure to materially greater environmental liability, personal injury and other claims for damages (including consequential damages), or the risk that the contract may be terminated by the government entity without cause on short-term notice, contractually or by governmental action, under certain conditions that may not provide us with an early termination payment. Should we enter into such contracts, we can provide no assurance that the increased risk exposure will not have an adverse impact on our future operations.

Risks Related to Our Financial Position and Capital Needs

As a newly public company with no revenue and operations, we will incur substantial operating losses for the foreseeable future and may never achieve or sustain profitability.

We may never achieve or sustain profitability. None of our mineral projects have commenced commercial production, and commercial production at our mineral projects will require significant capital and expenditures. To become and remain profitable, we must generate significant revenues at one or more of our mineral projects, which will require us to be successful in a range of challenging activities that are subject to numerous risks, including those set forth in this “Risk Factors” section. In addition, we may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors that may adversely affect our revenues, expenses and profitability. Our failure to achieve or sustain profitability would depress our market value, could impair our ability to execute our business plan, raise capital or continue our operations and could cause you to lose all or part of your investment.

Our ability to fund mineral exploration and development depends on our ability to obtain additional financing, and we may be unable to do so on favorable terms, if at all.

Mineral exploration and development are capital-intensive activities. Specifically, the exploration and exploitation of reserves, mining and processing costs, the maintenance of machinery and equipment and compliance with applicable laws and regulations require substantial capital expenditures. We will be required to make substantial expenditures for the continued exploration and, if warranted, development of our mineral properties. Mining industry development projects typically require a number of years and significant expenditures before production can begin.

Our current financial resources are limited and will be insufficient to fund all planned exploration, development, and general administrative expenses. To continue operations, we will need to raise substantial additional capital through equity or debt financings in the future. The ability to secure this capital is subject to numerous factors, including the success of our exploration efforts, the general state of the capital markets, and investor sentiment toward the rare earth elements industry. There is no assurance that future financing will be available when needed or that it will be on terms that are not highly dilutive to existing shareholders. Mineral projects could experience unexpected problems and delays during development, construction and start-up. We may not be successful in obtaining the required financing or, if we can obtain such financing, such financing may not be on terms that are favorable to us. Any failure to obtain sufficient equity or debt financing for our operations on favorable terms could have a material adverse effect on our financial condition, results of operations, and prospects.

We may experience time delays, unforeseen expenses, increased capital costs, and other complications while developing our projects, these could delay the start of revenue-generating activities and increase development costs. If we establish the existence of mineral reserves in our ongoing projects in a commercially exploitable quantity, we will require additional capital in order to develop the properties into producing mines. If we cannot raise this additional capital, we will not be able to exploit any reserves, and our business could fail.

The production of rare earth elements and mineral exploration and mining by their nature involve significant risks and hazards, including potential for adverse environmental impacts, as well as industrial and mining accidents. These include, for example, occupational hazards, leaks, ruptures, explosions, chemical spills, seismic events, fires, cave-ins and blockages, flooding, discharges of gasses and toxic substances, contamination of water, air or soil resources, unusual and unexpected rock formation affecting mineralization or wall rock characteristics, ground or slope failures, rock bursts, wildfires, radioactivity and other accidents, incidents, or conditions resulting from mining or manufacturing activities, including, among others, blasting and the transport, storage and handling of hazardous materials. These operations can be dangerous and safety incidents in these operations may cause damage to and loss of equipment, injury or death, monetary losses and potential legal liabilities. Any such incidents could have a material

17

adverse effect on our business, operating results and financial condition. Furthermore, there is the risk that relevant regulators may impose fines and work stoppages for non-compliant production or mining operating procedures and activities, which could reduce or halt production or mining until lifted. The occurrence of any of these events could delay or halt production, increase production costs and result in financial and regulatory liability for us, which could have a material adverse effect on our business, results of operations and financial condition. In addition, the relevant environmental authorities have issued and may issue administrative directives and compliance notices in the future, to enforce applicable statutes or regulations which may require us to implement, maintain, or complete specific environmental assessment, protection or remediation measures. The authorities may also order the suspension of part, or all, of our operations if there is non-compliance with applicable laws or regulations. Contravention of some of these statutes or rules may also constitute a criminal offense and an offender may be liable for a fine or imprisonment, or both, in addition to administrative penalties. As a result, the occurrence of any of these events may have a material adverse effect on our business, results of operations and financial condition.

We have no operating history on which to evaluate our business and performance, and accordingly, our prospects must be considered in light of the risks that any new company encounters.

We were re-incorporated under the laws of the State of Texas, effective as of October 15, 2025. We have never generated any revenue from operations, our mineral properties are in the exploration stage, and we have never produced minerals in commercial quantities from any of our mineral properties. We face many risks common to early-stage enterprises, including under-capitalization, cash shortages and limitations with respect to personnel and other resources. The likelihood that in the future we will generate a level of revenue to achieve and sustain profitable operations must be considered in light of the early stage of our operations.

There is no assurance that any of our mineral properties will ultimately produce minerals in commercially viable quantities or otherwise generate operating earnings. Advancing our mineral properties into the development stage will require significant capital and time, and successful commercial production from any mines on such properties will require us to complete feasibility studies to estimate the anticipated economic returns of a project, obtain adequate financing, obtain various permits, construct processing plants and infrastructure, and complete other activities. We may not succeed in establishing mining operations or profitably producing metals at any of our current or future properties.

A non-U.S. holder may be treated as having income that is “effectively connected” with a United States trade or business upon the sale or other taxable disposition of our common stock unless (i) our common stock is regularly traded on an established securities market and (ii) such non-U.S. holder did not meet certain ownership thresholds during the applicable testing period.

A Non-U.S. Holder (as defined below) of our common stock generally will incur U.S. federal income tax on any gain realized upon a sale or other disposition of our common stock to the extent our common stock constitutes a “United States real property interest” (“USRPI”) under the Foreign Investment in Real Property Tax Act of 1980 (“FIRPTA”). A USRPI includes stock in a “United States real property holding corporation” within the meaning of Section 897(c)(2) of the Code (a “USRPHC”). To our knowledge, we believe we currently are not a USRPHC. However, since the determination of whether we are or may become a USRPHC depends on the fair market value of our USRPIs relative to the fair market value of our non-U.S. real property interests and our other business assets, there can be no assurance we will not become one in the future.

Under the FIRPTA regime, a Non-U.S. Holder is taxed on any gain realized upon a sale or other disposition of a USRPI as if such gain were “effectively connected” with a United States trade or business of the Non-U.S. Holder. A Non-U.S. Holder thus will be taxed on such a gain at the same graduated rates generally applicable to U.S. persons. In addition, a Non-U.S. Holder will have to file a U.S. federal income tax return reporting that gain.

However, if our common stock is regularly traded on an established securities market (the “Regularly Traded Exception”), then gains realized upon a sale or other disposition of the common stock will not be treated as gains from the sale of a USRPI, as long as the Non-U.S. Holder owned, actually and constructively, 5% or less of our common stock throughout the shorter of the five-year period ending on the date of the sale or other taxable disposition or the Non-U.S. Holder’s holding period. It is uncertain whether a trading market for our securities may develop and whether our common stock will be regularly traded for purposes of the Regularly Traded Exception (see also our “There has

18

been no public market for our common shares prior to this offering, and an active market in which investors can resell their shares may not develop“ risk factor on page 28 of this prospectus). Accordingly, we can provide no assurances that the common stock will meet the Regularly Traded Exception at the time a Non-U.S. Holder purchases such security or sells, exchanges, or otherwise disposes of such security. The foregoing summary is qualified in its entirety by the discussion contained herein under the heading “Material U.S. Federal Income Tax Consequences to Non-U.S. Holders”.

Non-U.S. Holders should consult their own tax advisors regarding the potential application of the FIRPTA regime to their investment in our common stock.

We may experience increased costs at our mineral properties which could have a material adverse effect on our business, financial condition, results of operation and prospects.

The costs of exploring and developing our mineral properties will be subject to variation from time to time due to a variety of factors including

Costs are also affected by the price of commodities necessary for our operations such as fuel, steel, water, and electricity. Such commodities may be subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any of our four material mineral projects could have a material negative impact on our business, financial condition, results of operation and prospects.

Risks Related to the Rare Earth Elements Mining Industry

The mining industry is highly competitive.

The mining industry is highly competitive. Much of our competition will come from larger and more established mining companies that have greater resources than us, including more executive management and administrative personnel, more qualified employees, newer and more efficient equipment, lower cost structures, greater liquidity and access to credit and other financial resources, more effective risk management policies and procedures, and greater financial resources allowing for a greater ability to explore and develop mining properties and withstand potential losses. As a result of such advantages, some of our competitors may be able to (i) respond more quickly to new laws, regulations or emerging technologies, (ii) devote greater resources to the operation, expansion or efficiency of their operations, and (iii) expend greater amounts of resources, including capital, in acquiring new and prospective mining properties. In addition, current and potential competitors may make strategic acquisitions or establish cooperative relationships among themselves or with third parties; and the resulting competitors or alliances may gain significant market share to our detriment. We may not be able to compete successfully against current and future competitors, and any such failure to compete successfully could have a material adverse effect on our business, financial condition or results of operations.

China has historically been the largest producer of rare earth elements, controlling a significant portion of the global output, and as a significant player, China possesses great leverage in dealing with competitors in the industry, by among other things, manipulating pricing, processing speed and other factors.

19

China controls a substantial majority of the world’s rare earth elements production. China’s rare earth elements industry benefits from extensive government support, allowing Chinese companies to offer rare earth elements at subsidized prices, often undercutting other producers. Moreover, Chinese companies have invested heavily in improving their processing capabilities, giving them a technological and cost advantage in the global market. Since December 2023, China has banned the export of such technologies and capabilities. While geopolitical friction and U.S. tariff measures have tightened the pressure on China’s rare earth supply-chain leading position, weakening or displacing China’s preeminence in the sector will demand sustained, coordinated action and significant investment over an extended horizon.

Mining and mineral exploration is inherently dangerous and subject to conditions or events beyond our control, which could have a material adverse effect on our business and plans.

Mining and mineral exploration involves various types of risks and hazards, including:

These risks could result in damage to, or destruction of, our projects, production facilities or other properties, personal injury, environmental damage, delays in mining, increased production costs, monetary losses and possible legal liability. We may not be able to obtain insurance to cover these risks at economically feasible premiums. Insurance against certain environmental risks, including potential liability for pollution or other hazards as a result of the disposal of waste products occurring from production, may be prohibitively expensive. We may suffer a material adverse effect on our business if we incur losses related to any significant events that are not covered by our insurance policies.

Permitting, licensing and approval processes are required for our operations and obtaining and maintaining required permits and licenses is subject to conditions which we may be unable to achieve.

Both mineral exploration and extraction at our projects require permits from various federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. Please see the sections titled “Properties – Shiloh Project,” “Properties – Alpha Project,” and “Properties – Constellation Project” for a description of the permits known to be required. Such licenses and permits are subject to changes in regulations and changes in various operating circumstances. Companies such as ours that engage in exploration activities often experience increased costs and delays in production and other schedules because of the need to comply with applicable laws, regulations and permits. Issuance of permits for our activities is subject to the discretion of government authorities,

20

and we may be unable to obtain or maintain such permits. Permits required for future exploration or development may not be obtainable on reasonable terms or on a timely basis. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration or development of our projects (or any other mineral properties that we may subsequently acquire) or for the construction and operation of a mine on our properties that we may subsequently acquire at economically viable costs. If we cannot accomplish these objectives, our business could face difficulty and/or fail.

There may be defects in our rights under the mining claims that comprise our properties, and such defects could impair our ability to explore for mineralized material and to otherwise develop such properties.

The mining claims we rely on at our mineral properties may be challenged, and we may not have, or may not be able to obtain, the surface rights needed to explore for or develop any resources present at the property related to such claims. Unknown defects with respect to any of such claims could adversely affect our ability to explore and develop the property or process the minerals that we may ultimately mine at the applicable property. Title insurance for mineral properties is generally not available at a reasonable cost, and we may have limited ability to ensure that we have obtained valid rights to individual mineral properties. We rely on public records in Brazil with respect to our mining claims. However, any challenge to our rights in a concession could result in litigation, insurance claims and potential losses, hinder our access to capital, delay the exploration and development of the property and ultimately result in the loss of some or all of our interest in the related mineral project.

Mineral operations are subject to market forces outside of our control which could negatively impact our operations.

The marketability of minerals is affected by numerous factors beyond our control including market fluctuations, government regulations relating to prices, taxes, royalties, allowable production, imports, exports and supply and demand. One or more of these risk elements could have an impact on the costs of our operations and if significant enough, reduce the profitability of our operations.

Volatility in commodity markets may impair our financial results and access to capital.

Prices for minerals constantly fluctuate, and if the prices of rare earth elements (the primary minerals for which we are exploring) experience sudden or protracted declines, our exploration activities for those minerals may become unattractive and we may discontinue those activities. Prices of minerals are determined by a variety of factors, including market volatility in commodities prices; the exchange rate between the Brazilian Real and the U.S. Dollar; global and regional supply and demand; and changes or volatility in political and economic conditions and production costs in major mineral producing regions of the world.

Changes in government policies or funding priorities for rare earth elements and critical minerals could reduce or eliminate incentives, grants, or programs we rely on, adversely affecting development of our mineral projects and demand for our products.

Government policies regarding rare earth elements and critical minerals are subject to frequent changes based on national security priorities, supply chain assessments, and political considerations. Changes to critical minerals lists, or government funding priorities related to commercial facilities for the mining or manufacturing of rare earth elements or critical minerals, could affect our eligibility for government incentives, grants, or preferential treatment in government procurement. The modification of programs such as the Defense Production Act, the Infrastructure Investment and Jobs Act, or the Inflation Reduction Act could impact available funding, tax incentives, or regulatory streamlining that we currently benefit from or expect to benefit from in the future. Additionally, changes in government priorities or budget constraints could further result in the elimination or reduction of programs that support domestic rare earth elements and critical mineral production and processing. Further, cooperating nations’ governments may decrease support for rare earth elements and critical minerals, which could also adversely impact demand for our products and/or may pose permitting, financing and other risks for developing our projects.

Risks Related to Our Operations in Brazil

Changes in U.S. trade policy, including the imposition of tariffs on goods from Brazil, could materially and adversely affect our business and financial results.